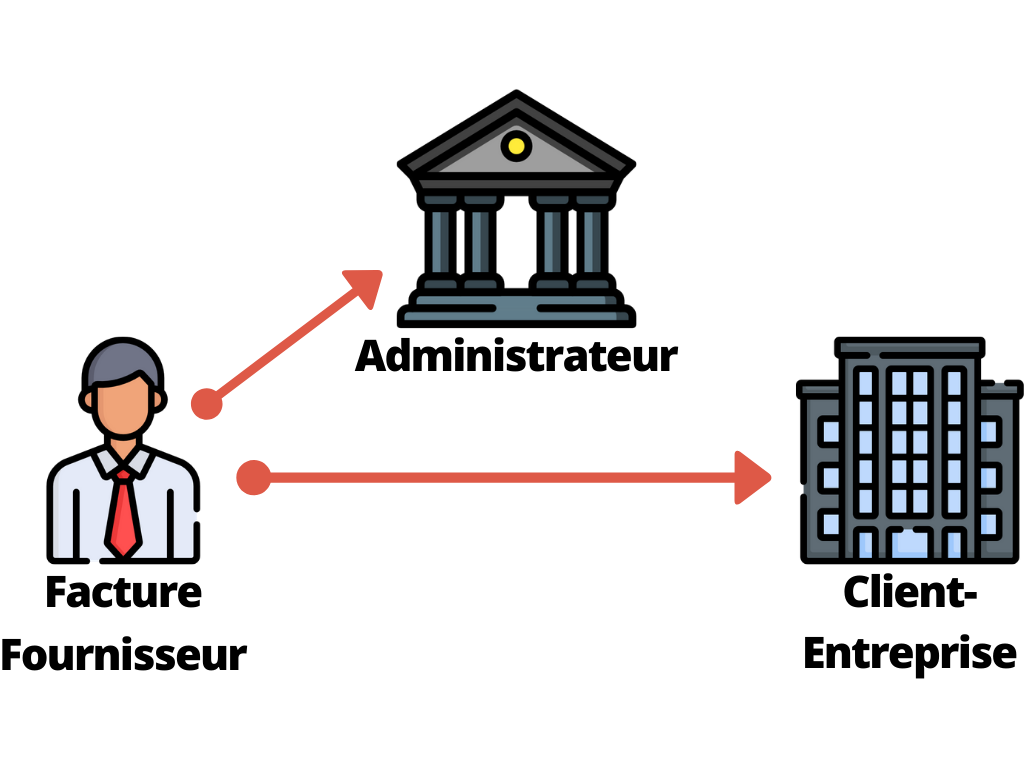

The transaction receipts between entities subject to VAT are issued in electronic form and the data are sent to Administration for processing: modernisation of data collection and VAT control issues.

The first subparagraph shall apply at the earliest from January 1st, 2023 and at the latest from January 1st, 2025, according to a schedule and terms fixed by decree depending on, among others, the size and sector of the companies concerned, and after obtaining the authorization provided for in Article 395.1 of the Council Directive 2006/112/EC of November 28, 2006 on the common VAT system.

The Government must submit to Parliament (before September 1st, 2020) a report on the conditions for implementing the obligation of electronic invoicing in inter-company relations, at the earliest from January 1st, 2023 and at the latest from January 1st, 2025. This report

identifies and assesses the most appropriate technical, legal and operational solutions, especially in terms of data transmission to Tax Administration, considering the operational constraints of the respective parties. It assesses, for every option, the expected gains in VAT collection and the expected benefits for the companies.

The Clearance model: this is a tripartite model between the seller, the buyer and the administration. Before issuing any invoice, the supplier of a good or service must wait for approval from the tax administration before billing the buyer. The issue of each invoice is declared and authorized by the tax authorities. Thus, the tax authorities know what amounts of VAT are collected. This model is already followed by many countries in South America, Russia and China.

In the Italian Clearance model, the State intervenes in the exchange of invoices between the supplier and the customer, via an exchange system called “Sistema di interscambio” (SDI). In return the supplier must affix to his/her invoice a code received from the Administration.

Moreover, each country announces specificities of its own. France may consider offering an online VAT pre-declaration service. The Tax Administration would thus have perfect visibility, in relation to the VAT collected by taxable entities, but that would also allow taxable entities to have a pre-filled version of the declaration form (type CA3 or equivalent).

Sébastien MINOTTI – Desktop-Publishing Expert

Fekra Digital Services, an entity of Fekra Global Services, is proud to announce that its Indian Arm Incorporation has been successful and we look forward to working closely with our team in India. With this our expansion plan has just begun and we expect to make more announcements like this one in the near future. […]

As soon as AI started emerging from the field of research, Banking became a particularly favourable development axis for it. The banking business has also accelerated the implementation of several applications linked to AI: Expert Systems, bank risk, Data Management, Regulatory… Wider process automation thanks to « Machine Learning » Thanks to ‘Machine Learning’, machines […]

Patches, version upgrades and functional changes represent the life cycle of information systems. In order to keep a high level of quality, it is essential to launch test campaigns every time you intervene on the system to ensure non-regression, not only functional but also technical. The automation of these tests will necessarily bring added value […]

Do not hesitate to contact us should you need any further information. Contact us